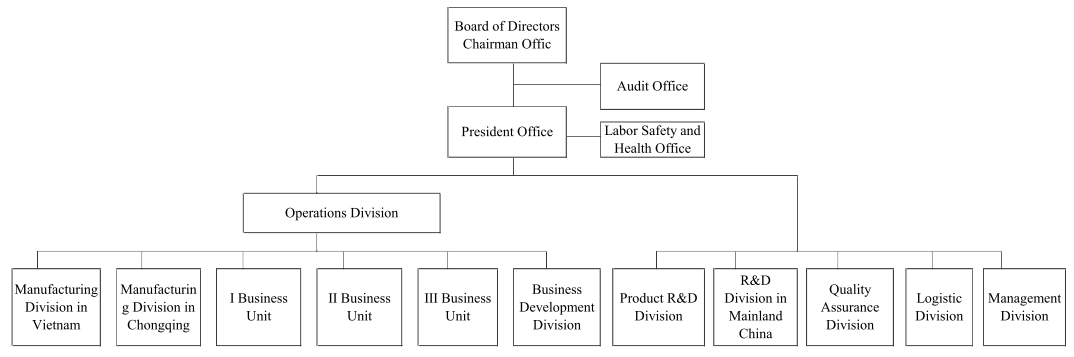

Functional Committee

Corporate governance structure

Functional Committees

Audit Committee

The Company’s Audit Committee consists of three independent directors and shall convene at least one meeting per quarter. The independent directors are responsible for the adequate expression of the Company’s financial statements, election (dismissal), independence and performance of CPAs, effective implementation of internal control, compliance with laws and rules and control over existing or potential risks. Their main responsibilities are described as follows:

- ◎ Establishment or amendment of the Company’s internal control system pursuant to Article 14-1 of the Securities and Exchange Act.

- ◎ Assessment of the validity of the internal control system.

- ◎ Establishment or amendment of the handling procedures regarding significant financial business behaviors, including the acquisition and disposal of assets, trading of financial derivatives, loaning of funds to others, and endorsement/guarantees for others in accordance with Article 36-1 of the Securities and Exchange Act.

- ◎ Matters involving any directors’ personal interests.

- ◎ Significant transactions of assets or financial derivatives.

- ◎ Significant loans of funds, and endorsement/guarantees.

- ◎ The offering, issuance, or private placement of equity-type securities.

- ◎ The hiring or dismissal of CPAs, or the compensation given thereto.

- ◎ The appointment or discharge of a financial, accounting, or internal audit officer.

- ◎ Annual financial statements

- ◎ Any other material matter required by the Company or the competent authority.

The Audit Committee held four meetings in the most recent year (2020). The attendance record of the independent directors is listed below:

| Title | Name | Actual attendance | Proxy attendance | Actual attendance rate (%) | Remarks |

|---|---|---|---|---|---|

| Independent Director | Ting Hung-Hsun | 4 | 0 | 100 | |

| Independent Director | Judy Y.C. Chang | 3 | 1 | 75 | |

| Independent Director | Lin Ying-Shan | 2 | 2 | 50 |

Other particulars:

- 1. Where the operations of the Audit Committee meet any of the following circumstances, the minutes concerned shall clearly state the meeting date, session, contents of proposals, resolutions made by the Audit Committee and the Company’s resolution of the Audit Committee’s opinions.

- (1) Matters specified in Article 14-5 of the Securities and Exchange Act.

If none of the independent directors objects or expresses qualified opinions to the proposals mentioned above, such proposals shall be approved unanimously by all attending members.

Meeting date (session) Proposal March 23, 2020

(1st meeting in 2020)Proposal of the Company's "Declaration of Internal Control System" Proposal of the 2019 financial statements May 11, 2020

(2nd meeting in 2020)Proposal of the 2019 business report Proposal for 2019 earnings distribution November 06, 2020

(4th meeting in 2020)Proposal for revision of the Company's "accounting system" Proposal of the 2021 audit plan Revision of the Company's "internal audit system," "internal control system_property, plant, and equipment cycle," "internal control system_financing cycle" Proposal for assessment of the independence of the Company's CPAs Proposal for determination of the significant amount for disguised financing - (2) Other than those described above, any resolutions unapproved by the Audit Committee but passed by more than two-thirds of all the directors: None.

- (1) Matters specified in Article 14-5 of the Securities and Exchange Act.

- 2. Independent directors’ avoidance of proposals involving any conflict of interest, information including the director’s name, contents of the proposals, causes of recusal, and participation in the voting process should be stated: None.

- 3. Communication of the independent directors with the internal audit officer and CPAs (e.g. the major matters, methods, and results of communication with regard to the financial and business affairs of the Company):

Policies of the communication between the independent directors and the internal audit officer: The internal audit officer shall submit audit reports to the independent directors on a regular basis and report the progress of the audit work thereto at least once per quarter. When any material irregularities occur, a report must be immediately prepared for review, and the independent directors shall be notified.

Policies of the communication between the independent directors and CPAs: CPAs shall meet with the independent directors at least once a year (at an Audit Committee meeting or a communication meeting) to report the Company’s financial position and internal control implementation to the independent directors and explain accounting practice principles and matters causing major impacts on profits or losses and any recent amendments to relevant laws and regulations. In case of any material circumstances, such meeting may be convened at any time.

Remuneration Committee

(1) The Company’s Remuneration Committee consists of three independent directors (Ted Lin, Judy Y.C.Chang and Hung-Hsun Ting).

(2) Term of office: 2018/06/22–2021/06/21. The Remuneration Committee convened two meetings (A) in 2020, and the attendance of the Committee members are listed as follows:

| Title | Name | Actual attendance (B) | Proxy attendance | Actual attendance rate (%) (B/A) | Remarks |

|---|---|---|---|---|---|

| Convener | Lin Ying-Shan | 1 | 1 | 50 | |

| Independent Director | Judy Y.C. Chang | 1 | 1 | 50 | |

| Independent Director | Ting Hung-Hsun | 2 | 0 | 100 |

Other particulars:

- 1. Scope of Duties of the Remuneration Committee:

- (1) Establish and periodically review the policies, standards and structure of the performance evaluation and remuneration for the directors and managers of the Company.

- (2) Regularly review and adjust the remunerations to the directors and managers.

- 2. If the Board of Directors does not adopt or amend the suggestions from the Remuneration Committee, the date and session of the Board meeting, contents of the proposals, meeting resolutions, and the Company’s handling of the Remuneration Committee’s opinions shall be specified (if the remuneration passed by the Board of Directors is higher than that suggested by the Remuneration Committee, the deviation and causes thereof shall be specified): None.

- 3. If any member objects or expresses qualified opinions to the resolution made by the Remuneration Committee, whether on-the-record or in writing, the date and session of the meeting, contents of the proposal, the entire members’ opinions, and how their opinions are addressed shall be specified: None.

Meeting date (session) Proposal March 23, 2020

(1st meeting in 2020)Proposal for distribution of the remuneration to employees in 2019 November 06, 2020

(3rd meeting in 2020)Proposal of the bonus to managers in 2020